Asia Securities’ latest report quantifies COVID-19 impact on key economic variables in Sri Lanka

Published on 24 April, 2020

Share this on:

The ongoing novel coronavirus (COVID-19) outbreak will clearly have a significant impact on the Sri Lankan economy. In the backdrop of a recessionary impact on output (GDP) the more visible impact would manifest itself through supply chain disruptions, sharp declines in domestic demand, a high fiscal deficit given lower government revenue, low tourism revenue and remittances, and a weakening LKR/USD rate, according to a new analysis by Asia Securities, a leading investment firm in Sri Lanka.

Asia Securities’ Macroeconomic Update last month explored a range of scenarios with assigned probabilities to estimate COVID-19’s impact on Sri Lanka’s GDP; the most probable case forecasts a GDP contraction of 4.0-.5% in real terms. However, the impact could change depending on how the outbreak evolves as there are several unknowns affecting forecasts at this point of time.

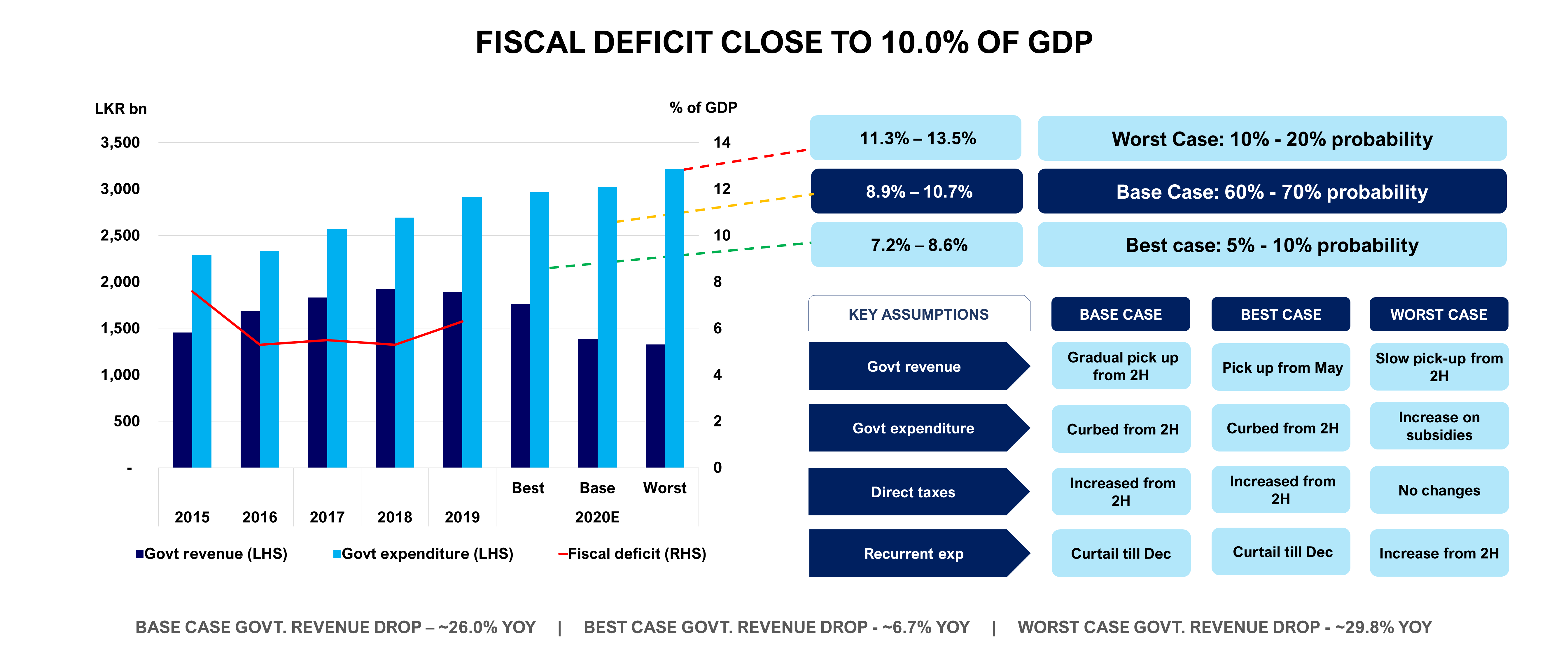

Following the GDP analysis published last month, the latest Macroeconomic Update looks at the impact of the outbreak and subsequent social-distancing measures on other key macro-variables. The analysis indicates that the largest challenges tothe economy stems from (i) a high fiscal deficit, (ii) weakening USD/LKR rate, (iii) pressure on the current account, and (iv) high debt/GDP.

In the base case scenario, where the virus containment could happen by end May (60-75% probability), Asia Securities forecasts fiscal deficit (as a percentage of GDP) could rise to 8.9–10.7% in 2020 from 6.5% in 2019. Despite the government’s measures to curb expenditure, low government revenue is expected to contribute to high fiscal deficit.

Although the report projects that the trade balance will worsen, the temporary import restrictions which are expected to last 3-5 months and low global oil prices may help contain the trade deficit to some extent this year, amid significantly low export demand.

On the reserves front, Sri Lanka is expected to receive some support from foreign funding in the form of IMF funding and new multilateral bilateral loans. However, slow forex inflows from remittances and tourism may hamper reserves, weakening it to 3.2–3.8 months of imports.

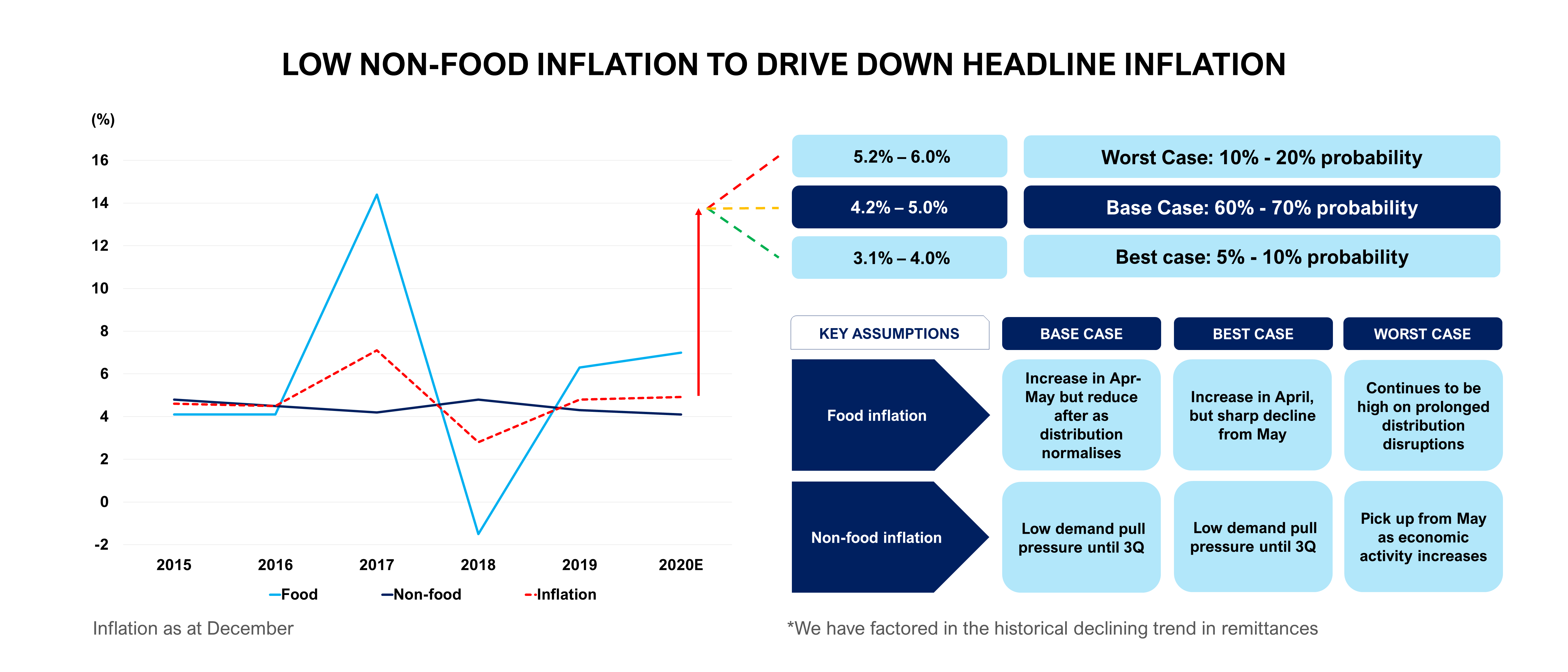

On the positive side, the report suggests that inflation will taper offin 2020 as a result of lower demand side pressure. While food inflation could remain high in 1H 2020, this would normalise in 2H 2020.

Asia Securities’ Economist Lakshini Fernando notes that “While there are several uncertainties about COVID-19 outbreak and its economic impact, we hope that our analysis which offers a range of scenarios can better equip Sri Lankan businesses looking to navigate this tumultuous period.”

The analysis titled ‘Asia Securities Macro Economic Update: Forecast for Key Economic Indicators’ aims to quantify the impact of the coronavirus pandemic on USD/LKR, bond yields, reserves, fiscal balance, trade balance, current account, inflation and debt/GDP. A full breakdown of all scenarios and assessments are available to Asia Securities’ client via the Research Portal or their investment advisor, and will be updated as the situation evolves.

Trending Articles

About the author